Learn why circular lending strategies in DeFi are dangerous and how they can lead to cascading liquidations and massive losses.

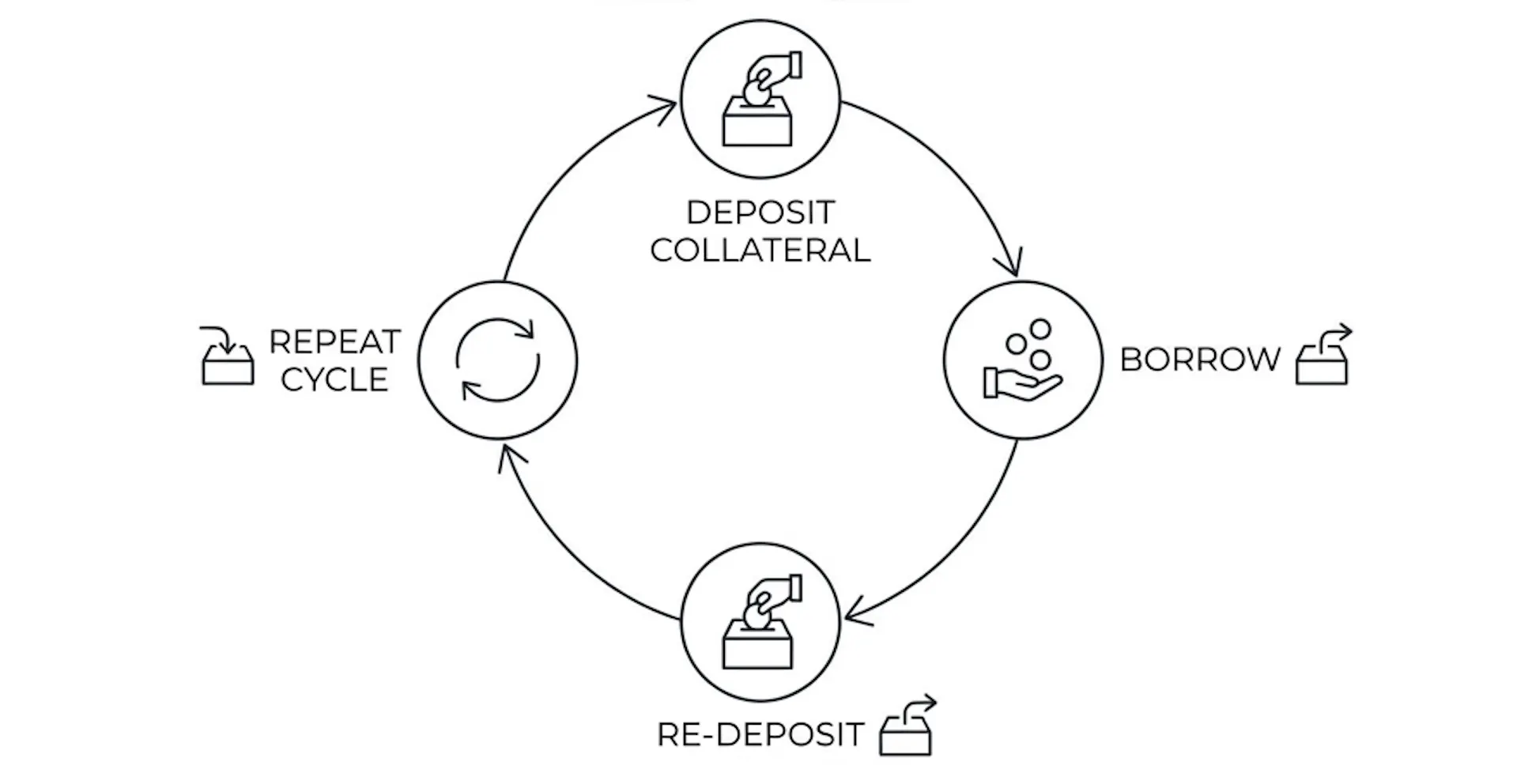

Circular lending and borrowing (also known as looping or recursive lending) is a DeFi strategy where users repeatedly deposit an asset as collateral, borrow against it, and re-deposit the borrowed funds into the same or another lending protocol.

Through multiple loops, users can significantly increase their apparent deposit size and borrowing volume, despite starting with a relatively small amount of capital. This technique is commonly used to:

At its core, circular lending is a self-managed leverage strategy implemented on-chain.

Assume the following setup:

| Parameter | Value |

|---|---|

| Initial capital | 10,000 USDC |

| Lending protocol LTV | 75% |

| Deposit sUSDE APY | 5% |

| Borrow USDC APY | 3% |

Swap 10,000 USDC to 10,000 sUSDE (assume 1:1 ratio), then deposit 10,000 sUSDE and borrow 7,500 USDC.

Swap 7,500 USDC to 7,500 sUSDE, re-deposit 7,500 sUSDE, and borrow 5,625 USDC.

Swap 5,625 USDC to 5,625 sUSDE, re-deposit 5,625 sUSDE, and borrow 4,218 USDC.

| Metric | Value |

|---|---|

| Total deposits | 23,125 sUSDE (earning 5% APR) |

| Total borrows | 17,343 USDC (paying 3% APR) |

| Net yield per year | (23,125 × 5%) - (17,343 × 3%) = $635.46 |

| Total capital at risk | 10,000 - 4,218 = $5,782 |

| Final APR | 10.99% |

After three loops, we increase the sUSDE 5% APR yield to 10.99%. But if sUSDE price drops to 0.75 (perhaps due to a hack on-chain or CEX issue), the money we deposited will all be gone.

While capital efficiency improves, risk grows much faster than yield.

While circular lending can look attractive on the surface, its risk–reward profile is often asymmetric: limited upside with amplified downside.

In many cases, the net yield from circular lending is marginal:

However, every additional loop increases leverage multiplicatively, meaning that a small adverse change can wipe out a disproportionately large position.

Example: Assume a circular DAI position spans three different protocols, and each protocol independently carries a 1% failure risk.

The combined risk is: 1 - 0.99³ ≈ 3%

As more protocols are involved, risk compounds, while yield does not. Adding one more protocol does not double returns, but it does increase systemic exposure.

Risk scales faster than reward.

Liquidation risk is the most direct and destructive threat:

Because all positions are tightly coupled, circular lending has far less margin for error than simple collateralized borrowing.

Black swan events happen every year — sometimes multiple times per year:

| Date | Event | Impact |

|---|---|---|

| May 2022 | UST collapse | Cascading liquidations across DeFi |

| Mar 2023 | Silicon Valley Bank failure | USDC depegged to ~$0.93 |

| Feb 2025 | Bybit exploit | USDe temporarily lost its peg |

| Oct 2025 | Market crash | Triggered by macro and tariff-related news |

Systemic risk is permanent. Crypto liquidity is far more fragile than most users expect.

Even for high-market-cap assets like Bitcoin or Ethereum, 30% single-day drops occurred around 2020. Even in 2026, with improved liquidity, ±5% daily moves are still possible. With high leverage, liquidation is often a matter of when, not if.

Interest rates in DeFi are dynamic and utilization-based. Risks include:

A position that was profitable at block N can quietly become negative carry hours later, especially during market stress.

That said, interest rate risk is usually the smallest among all risks. In the worst case, it typically results in reduced DeFi income or moderate losses. It is rarely catastrophic by itself — but it can worsen other risks.

Circular lending concentrates exposure into a fragile dependency chain:

This is a tightly coupled system — failure at any single point can destabilize the entire loop.

For example, a smart contract issue can trigger panic withdrawals. Liquidity exits lead to asset sell-offs, which then feeds back into liquidation and liquidity risk. Many historical lending exploits disproportionately harmed users running recursive strategies.

Circular lending is not inherently wrong, but it should be treated as a high-maintenance, high-risk strategy — not passive yield.

Oracle anomalies are a common trigger for unexpected liquidations.

Manual monitoring is often insufficient. At minimum, users should be able to:

Advanced users rely on scripts to adjust leverage, repay debt, and exit positions automatically. With modern "vibe coding," running a 24/7 monitoring bot costs only a few dollars per month — a small price to protect large positions.

(DeFi Sentinel is expected to provide Telegram-based notifications for real-time risk signals in the near future.)

Key metrics to watch:

| Metric | Why It Matters |

|---|---|

| Borrow APY vs Deposit APY | Determines net profitability |

| Utilization ratio | High utilization = volatile rates |

| Incentive emission schedules | Know when rewards expire |

Circular lending only works when rate conditions remain favorable — which is rarely guaranteed.

Low trading volume and thin liquidity increase systemic risk:

Prefer protocols with:

Borrowing high-quality assets such as USDT or USDC reduces tail risk. For large capital, diversifying across multiple liquidity pools further lowers exposure.

Circular lending and borrowing in DeFi is best understood as leveraged yield engineering, not free money.

For most users:

Unless you have strong risk controls, automated monitoring, and a clear understanding of the mechanics involved, circular lending strategies are likely to underperform simple, unleveraged positions over the long term.

The best yield strategy is often the one you can sleep through.

Circular lending — also called recursive borrowing or looping — is the practice of supplying an asset as collateral, borrowing against it, swapping the borrowed funds back into the original asset, supplying again, and repeating. Each loop magnifies effective exposure and yield, but it also magnifies losses, liquidation risk, and concentration in a single lending market.

The loop multiplies your exposure to one asset and one lending market simultaneously. A 5% adverse price move on the collateral can wipe out a 5x looped position because effective leverage compounds with each loop. Worse, a single bad oracle print or liquidity event can trigger cascading liquidations across every layer of the loop in a single block.

When the collateral price drops, the outermost loop hits its liquidation threshold and is sold by liquidators. The forced sale depresses the price further, pushing the next loop into liquidation, and so on. In thinly traded pairs this can spiral within minutes. The 2022 stETH/ETH discount and the 2023 USDC depeg are textbook examples of cascading liquidation events.

They are closely related but not identical. Leveraged looping describes the mechanic; circular lending describes the position structure (lend → borrow → swap → lend again on the same protocol). Some integrated products — for example leveraged LST vaults — automate the loop into a one-click deposit, hiding the risk profile from users rather than removing it.

For experienced users with strict position sizing, tight monitoring, and highly correlated pairs (e.g., wstETH/ETH), modest looping at 1.5x-2x is defensible. The real danger is leverage products that quietly run 5x-10x on volatile pairs. As a rule, if you cannot recite each layer's liquidation threshold and the unwind path from memory, you should not be looping.

Experienced team of blockchain researchers and analysts dedicated to making DeFi accessible to everyone.